- May 6

- 9 min read

XTech Flow Case Study | May 4–5, 2026 | GME (Primary) / EBAY (Secondary)

Table of Contents:

GME / EBAY Acquisition Announcement Flow Signal Summary

GME exhibited the most extreme single-session institutional distribution in the 60-day observation window on May 4, 2026 — a Z-score of −3.84 on net daily institutional flow of −$381.1M — in the session immediately following GameStop's unsolicited $55.5 billion acquisition proposal for eBay.

Detrended cumulative institutional flow collapsed from a 60-day peak of +$446M (recorded on May 1, one trading session before the announcement) to +$54M by the close of May 4, representing an 88% unwind in a single session.

This case study examines what the 1-minute flow decomposition across both the acquirer (GME) and the target (EBAY) reveals about how institutional capital priced deal-completion probability relative to the market-implied level embedded in each stock's price reaction.

The divergence between institutional and retail flows on May 4 was the widest in the observation window on both tickers and constitutes one of the cleanest informed/uninformed capital separation events in the dataset.

Flow Data Snapshot — GME/EBAY Key Inflection Points

The seven events below represent the statistically significant inflection points in the May 1–5 window across both tickers. The intraday charts carry the timeline; these cards isolate the signal content.

Central finding: institutional capital on GME moved from a cycle peak to near-zero detrended positioning in four trading sessions — including an intraday drawdown of $305M within the May 4 session alone — while retail flow on the same name moved in the opposite direction with equal statistical extremity.

On EBAY, the flow structure is distinct but complementary: institutions distributed into the news-driven gap, re-entered briefly in a mid-session arb window, then executed their most aggressive minute-level sell in the full 60-day dataset before completing the exit on May 5.

A. Institutional Flow Regime

The GME institutional flow regime across the observation window describes a textbook accumulation-to-distribution arc. From April 7 through May 1, detrended cumulative institutional flow rose from approximately +$169M to the cycle peak, with notable accumulation episodes on April 22 (Z: +2.06, net +$195.4M) and the final session of the buildup on May 1 (Z: +3.74, net +$306.2M). The April 22 session marked the first statistically significant accumulation event in the window; the May 1 session — which occurred one trading day before the acquisition bid was publicly reported — carries the most signal content. A Z-score at that level on the final pre-announcement session is consistent with informed pre-positioning, though the 60-day window cannot rule out coincidental factor exposure from unrelated systematic rebalancing.

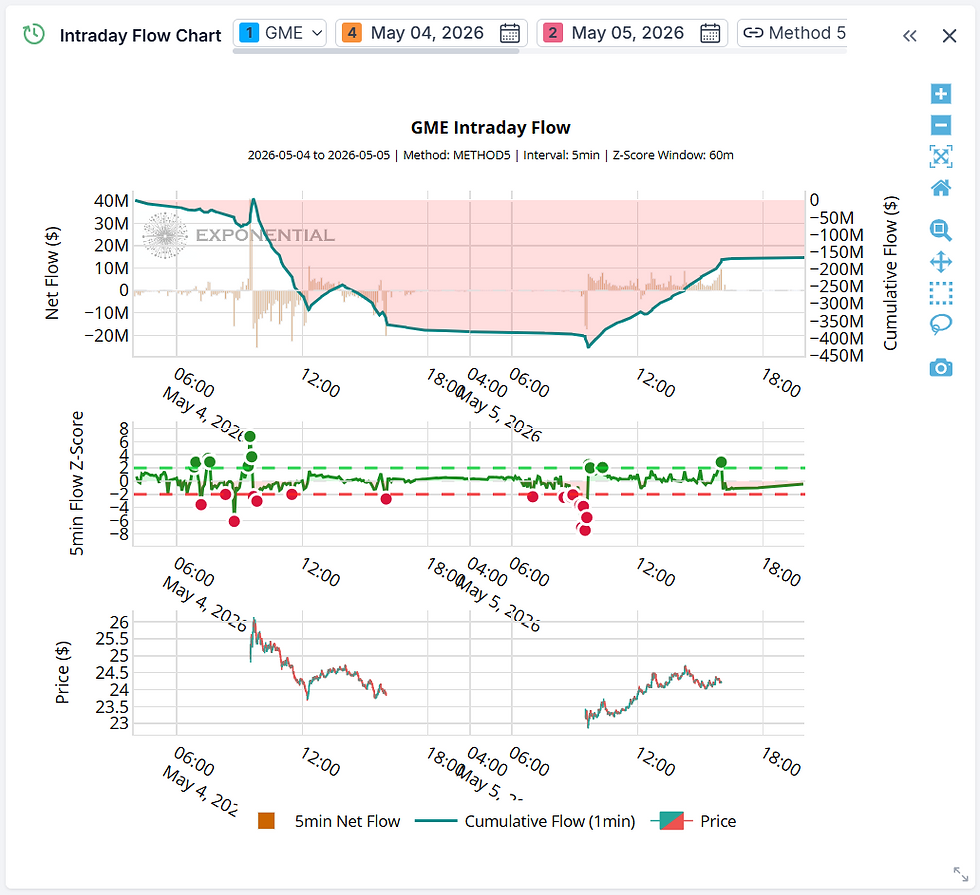

The May 4 distribution is unambiguous in magnitude and speed. The intraday decomposition adds critical texture: the opening 1-minute institutional buy (Z: +6.24, net +$20.8M) is consistent with pre-positioned longs exiting into the initial news-driven gap, not with new capital entering. Sustained distribution then ran throughout the session, with notable acceleration at 11:31–11:33 (Z: −4.37, −4.05), a sharp block at 14:03 (Z: −5.06), and heavy close-of-day selling at 16:00 (Z: −4.30, net −$7.1M). The day's institutional detrended cumulative flow moved from +$318M at the open to +$12.3M by the close.

The partial May 5 re-entry (Z: +2.22, net +$214.6M) is ambiguous but notable. The detrended cumulative flow recovered to +$242M from the May 4 trough, suggesting either fresh event-driven positioning by managers who view the deal as unlikely to close but the underlying equity as mispriced on a standalone basis, or tactical arb capital entering the acquirer side of the spread. The two hypotheses are not distinguishable within this dataset.

B. Retail-Institutional Divergence

The May 4 divergence on GME is the widest in the observation window by both Z-score differential and absolute dollar ratio. The 15.7:1 ratio of institutional selling to retail buying produced a textbook liquidity dynamic: retail absorbed a meaningful portion of the institutional order, but its capacity to clear $381.1M in net institutional supply was structurally limited.

The intraday retail pattern adds nuance that the daily aggregate obscures. At 09:31, retail posted a 1-minute Z of −7.33 — the highest-magnitude retail observation in the window — representing a brief sell-the-news reaction at the open. Within two minutes, retail flow reversed sharply (Z: +3.06 at 09:33), and by midday the buying had accelerated into waves (Z: +3.96 and +4.81 at 12:19–12:20). The intraday retail cumulative flow moved from a net sell at the open to a cycle high of +$24.0M by the close — the meme-stock community absorbed institutional distribution across the full session, with heaviest accumulation occurring in the final two hours as the stock continued to decline.

On EBAY, the divergence structure reveals a different dynamic. Retail opened the session as buyers (1-minute Z: +4.50 and +4.01 at 09:31–09:32), responding to the announced premium. Institutional flow was negative from the first minute. The 14:55 moment — institutional Z: −6.76 on −$25.5M against simultaneous retail Z: +7.15 on +$929K — is the most acute single-minute expression of divergence in the dataset. Retail was chasing a spread that institutional capital was actively collapsing. The dollar ratio at that specific minute was 27.5:1 of institutional selling to retail buying.

C. Cumulative Flow Interpretation

The peak-to-trough swing on GME institutional detrended cumulative flow — from the cycle peak of +$446M to +$54M on May 4 — represents a $392M drawdown across three trading sessions, with $305M of that concentrated intraday on May 4. The rolling 60-day regression removes secular drift; what remains isolates event-driven cyclical repositioning. The speed of the unwind — 88% of a 28-session accumulation reversed in one session — is statistically unusual within this observation window and consistent with a high-conviction directional exit rather than routine portfolio rebalancing.

The May 5 partial recovery to +$242M is insufficient to characterize the regime as re-accumulation. The detrended cumulative flow remains 46% below the pre-announcement peak, and the May 5 re-entry Z-score (+2.22) sits below the threshold of the accumulation sessions that built the April position. Caution is warranted in interpreting this recovery as a positive conviction signal.

On EBAY, the two-day institutional detrended cumulative flow swing from +$244M (May 1) to −$245M (May 5) — a $489M movement — represents the fastest-moving directional repositioning in the EBAY series within the window. The fact that the EBAY series turned negative simultaneously with the GME series stabilizing is consistent with capital migrating from an arb entry to a completed exit, rather than with a fundamental re-rating of EBAY's standalone value.

For Quant Portfolio Managers

Signal construction relevance.

The GME May 4 event is directly relevant to event-driven signal frameworks operating on institutional detrended cumulative flow momentum.

The accumulation arc from April 22 through May 1 would have generated a positive signal in any factor model with a lookback of five sessions or more.

The announcement-day reversal represents a near-instantaneous regime change: a 28-session buildout unwound in less than seven hours.

This highlights a structural limitation in flow-momentum signals without event-detection overlays — the factor is information-rich in trending regimes but carry-negative at event boundaries when institutional positioning built on private or semi-public information collapses simultaneously with price.

The May 4 data is consistent with an L/S flow momentum strategy being short-squeezed on the announcement gap before institutional distribution gave the short side a significant recovery.

Timing properties.

The gap between the detectable pre-event institutional flow inflection (May 1 peak, Z: +3.74) and the primary price move (May 4, −10.1%) is two trading sessions.

This is too short for most daily systematic strategies to act on directionally, but it is consistent with high-frequency event risk models that screen for unusual pre-announcement Z-score elevation as a risk flag.

More actionable is the intraday signal: the opening 09:31 institutional buy spike (Z: +6.24) decayed to sustained net negative within three minutes.

In a real-time flow framework, this flip — from extreme institutional buy at open to sustained institutional sell — represents a sub-five-minute signal that the opening gap is being sold by informed holders, not accumulated by new entrants.

Cross-sectional context and backtestable hypothesis.

The EBAY complementary flow — specifically the 14:55 crossover at Z: −6.76 vs. +7.15 — creates a cross-sectional deal-arb signal with potential generalizability.

Hypothesis for validation: in unsolicited acquisition announcements where the acquirer's stock declines more than 5% on the announcement day, the institutional detrended cumulative flow on the target crosses from positive to negative territory within two sessions in the majority of cases where the bid is ultimately rejected or withdrawn. If confirmed, this would provide a flow-based early signal of deal failure probability that leads the options market's implied probability by one to three sessions.

Secondary hypothesis: the magnitude of the acquirer's institutional flow reversal on announcement day (as measured by peak-to-trough detrended cumulative flow swing) is a negative predictor of deal-completion probability, independent of the target's price reaction to the announcement premium.

Risk and noise considerations.

GME's elevated retail participation creates moderately higher trade classification uncertainty relative to S&P 500 large-cap names.

The extreme retail Z-scores observed on May 4 (daily: +6.94; intraday open: −7.33) may partially reflect classification noise rather than clean retail signal, though the directional content is consistent across both daily and intraday series.

Post-announcement options activity and convertible arbitrage flows may also complicate the institutional/retail decomposition in names with atypical capital structure events.

For Fundamental Investors

Over the 60-day window ending May 5, GME institutional detrended cumulative flow built from approximately +$169M in early April to the cycle peak on May 1, then collapsed to +$54M on announcement day before recovering to +$242M on May 5. The core observation: institutional conviction on GME, as measured by the detrended series, was consistently net positive from April 7 through May 3. It turned sharply negative on the announcement and had not recovered its prior peak as of the close of this observation window.

The partial May 5 re-entry is insufficient to signal a new accumulation regime. Fundamental investors tracking institutional positioning as a sentiment indicator should note that the detrended cumulative flow — a more stable measure than daily net flow — remains 46% below the pre-announcement peak. Flow conditions consistent with renewed institutional conviction would require multiple consecutive sessions of Z-scores above +1.5 with an upward-sloping detrended cumulative trajectory, none of which had materialized by May 5.

On EBAY, the flow data offers an independent read on deal-completion probability that complements the spread analysis. The EBAY spot price on May 4 closed at approximately $109 against a $125 offer and a prior close near $104 — implying roughly a 24% deal-completion probability on a simple spread basis. Institutional flow data is consistent with a materially lower assessment: the institutional detrended cumulative series moved from positive to negative within two sessions, and the scale of the May 5 exit (−$327.5M, Z: −1.68) suggests the arb position built on announcement day was substantially unwound. Flow conditions that would indicate a change in institutional deal assessment — specifically, sustained institutional re-entry into EBAY with positive detrended cumulative flow trajectory — had not been observed as of the observation window's close.

Methodology Note

Data source.

XTech Flow data is derived from LSEG Data Analytics, aggregated to 1-minute intervals. The observation window covers April 7 through May 5, 2026, comprising 22 trading sessions. Z-scores and detrended cumulative flows are constructed against a 60-day rolling baseline; the window used here is a subset of that baseline.

Flow decomposition.

The proprietary classification algorithm separates institutional buy-side, market-maker, and retail flow using microstructure features derived from 20+ years of HFT expertise. Classification accuracy is higher for large-cap, high-liquidity names. GME's historically atypical retail participation profile and elevated order flow complexity introduce moderately higher classification uncertainty than is present in S&P 500 large-cap benchmarks — this should be factored into any interpretation of extreme GME retail Z-scores.

Z-score construction.

Z-scores are standardized against the 60-day rolling distribution of daily net flows for each investor type and ticker independently. Values beyond |2.0| represent statistically infrequent events within that specific name's recent history — these are relative, name-specific thresholds, not universal bounds. Cumulative flows are detrended to remove secular drift and isolate cyclical positioning changes.

Limitations explicitly stated.

The May 1 pre-announcement institutional flow elevation (Z: +3.74) is consistent with but does not confirm informed pre-positioning — systematic rebalancing or coincidental factor exposure cannot be excluded.

Extreme intraday Z-scores in GME carry higher classification noise than in liquid large-cap names.

The partial May 5 institutional re-entry cannot be attributed to a specific investor type or motivation within the current dataset.

Past flow patterns do not constitute predictive claims.

Signal Summary for Distribution: GME / EBAY Flow Intelligence Summary — May 4–5, 2026

Observation window: April 7 – May 5, 2026 | 22 sessions

Key finding:

GME institutional detrended cumulative flow collapsed 88% from its 60-day peak (+$446M → +$54M) on the acquisition announcement day (May 4), while retail simultaneously posted its most extreme net buy session in the window (Z: +6.94), producing a 15.7:1 institutional-to-retail selling ratio.

EBAY institutional flow turned the 60-day detrended cumulative series negative (−$245M) by May 5, consistent with rapid institutional repricing of deal-completion probability materially below the ~24% implied by the spot-to-bid spread.

GME institutional flow regime: Reversal — accumulation-to-distribution Peak detrended cumulative flow (GME): +$446M, May 1 (one session pre-announcement)

Peak divergence event: May 4, GME — institutional Z: −3.84 / retail Z: +6.94 (daily); EBAY 14:55 — institutional Z: −6.76 / retail Z: +7.15 (1-minute)

Hypothesis for validation: In unsolicited acquisition announcements with >5% acquirer-side price decline on announcement day, institutional detrended cumulative flow on the target reverses from positive to negative within two sessions when institutional deal-completion probability diverges materially from the market-implied spread probability.

Data: XTech Flow™ US Equity Flow Analytics | 1-min granularity | LSEG Consolidated Feed

Our research shows what really moves stock prices

For decades, asset pricing has been dominated by fundamentals. New research proves this view is incomplete.

The primary mechanical driver of stock prices is not fundamentals, but the force of institutional order flows.

Comments