- Dec 31, 2025

- 14 min read

When Meta announced its acquisition of Manus AI for more than $2 billion on December 29, 2025—the fastest-growing AI startup in history, reaching $100 million ARR in just eight months—the stock market did something strange: almost nothing.

Not euphoria.

Not a rally.

Barely moved. Stock gained just 1.1% to close at $665.95 on December 30 while the broader S&P 500 fell 0.14% and the Nasdaq dropped 0.24%.

But here's what makes this muted reaction fundamentally different from every other multibillion-dollar AI acquisition you've seen this year: Institutions sold the news before it was news.

On December 19, 2025—approximately 10 days before the public announcement, when Bloomberg later revealed the deal negotiations likely began—META stock was trading around $660-670. Retail investors were buying modestly, anticipating year-end momentum.

Institutions were selling explosively. -$6.24 billion in daily net flow with a Z-score of -2.74—meaning institutional selling was 2.74 standard deviations above normal. This wasn't routine profit-taking. This was the 99.7th percentile of distribution intensity.

Then came December 29. The deal dropped late in the day: Meta acquiring Manus—the Singapore-based, Chinese-founded AI agent startup hailed as "the next DeepSeek"—for more than $2 billion. The transaction was struck in about 10 days, according to Bloomberg. Manus would discontinue all China operations and buy out all Chinese investors to satisfy U.S. regulators.

The stock gained 1.1%.

Why so little on such massive news? Because institutions had already positioned. The smart money sold December 19 when deal negotiations started, distributing into retail buying. By the time the announcement became public, the information was already priced in.

Don't Trade on Headlines. Trade on Flows.

The Setup: From Chatbots to Action—Meta's $2 Billion Bet on AI Agents

Meta's December 29 announcement delivered far more than just another AI acquisition. The company secured Manus AI—a revenue-generating, product-market-fit-validated AI agent platform with explosive growth metrics that put it in a class by itself.

The Manus Story:

Launched in March 2025, Manus became the fastest startup in history to reach $100 million in annual recurring revenue—achieving this milestone in just eight months. Total revenue run rate exceeded $125 million by mid-December, with monthly growth above 20% since the release of Manus 1.5 in October.

The company:

Processed more than 147 trillion tokens

Created over 80 million virtual computer instances

Served millions of users across Brazil, the United States, Japan, and the Middle East

Employed just 105 people across Singapore, Tokyo, and San Francisco

Previously raised $75 million from Benchmark at a ~$500 million valuation in April 2025

Manus claimed to outperform OpenAI's DeepResearch and went viral immediately after internal testing began on March 6. Chinese state television cheered it as "China's next DeepSeek." Within one day of limited release, the product's internal testing codes were selling for 50,000 yuan ($7,000) on secondary markets.

The Technology:

Unlike Meta AI's conversational chatbots, Manus built true agentic AI—autonomous systems capable of executing complex, multi-step tasks without human intervention. Users could delegate entire workflows:

Resume screening and candidate evaluation

Trip itinerary planning with real-time booking

Stock portfolio analysis with actionable recommendations

Code debugging and full-stack application development

Market research and competitive analysis

This wasn't AI that responds to prompts. This was AI that executes tasks independently—the critical difference between "thinking" and "doing."

The Geopolitical Complexity:

Manus was founded in Beijing and Wuhan in 2022 by Butterfly Effect Technology before relocating headquarters to Singapore in mid-2025 to navigate U.S.-China tensions. The company's earlier funding from Tencent, ZhenFund, and HSG (formerly Sequoia Capital China) triggered scrutiny from U.S. Senator John Cornyn, who publicly criticized Benchmark's $75 million investment after the April 2025 funding round.

To close the Meta deal, Manus agreed to:

Discontinue all services and operations in China

Eliminate all continuing Chinese ownership interests

Shelve plans for a China-market product version

Buy out all Chinese investors completely

"There will be no continuing Chinese ownership interests in Manus AI following the transaction," a Meta spokesperson confirmed to Nikkei Asia.

This marks one of the first major instances of a U.S. tech giant acquiring a company with Chinese roots—and doing so by completely severing those ties to satisfy Washington.

The Strategic Timing:

According to Bloomberg, the agreement was struck in about 10 days—one of the fastest major tech acquisitions on record. Negotiations began around December 19-20 and concluded by December 29.

This speed matters because it reveals when informed capital knew. The deal wasn't rumors or speculation—it was active negotiation requiring institutional awareness. And the flow data shows exactly when that awareness translated into action.

The WhatsApp Monetization Inflection: Why Manus Changes Everything

Meta's valuation debate hinges on a single question: Can the company translate $70-72 billion in 2025 capital expenditures and $155 billion in projected 2026 operating expenses into tangible returns?

The Bullish Case:

Manus provides the execution layer Meta has been missing—the bridge between conversational AI and revenue generation. This solves Meta's most pressing strategic challenge: WhatsApp monetization.

WhatsApp has more than 3 billion monthly active users but has historically been a cost center, not a revenue driver. The platform's massive scale creates infrastructure expenses without proportional income. Meta AI, available across WhatsApp, Facebook, Instagram, and Messenger, drives user engagement but doesn't directly generate subscription or transaction revenue.

Manus changes that equation:

Small and Medium Business (SMB) Automation:

Manus fits "really beautifully" into WhatsApp's growing SMB footprint, according to Rosenblatt Securities analyst Barton Crockett. The platform already supports:

Click-to-WhatsApp ads (revenue-generating)

Business messaging features (paid)

Payment processing (enabled in select markets)

Business voice calling (recently launched for large enterprises)

With Manus integrated, businesses can deploy "digital employees" that:

Handle customer service inquiries 24/7 without human labor

Process orders and payments within chat

Provide personalized product recommendations

Manage inventory and scheduling autonomously

Scale conversations from dozens to thousands simultaneously

This creates a subscription-based revenue model: businesses pay Meta for AI agent capabilities, transforming WhatsApp from infrastructure cost into profit center. With 200 million WhatsApp Business users already on the platform, the addressable market is massive.

Competitive Moat:

Meta banned general-purpose third-party AI chatbots from WhatsApp Business effective January 15, 2026, clearing the field for Meta AI as the exclusive assistant. By owning both the platform (WhatsApp) and the agent technology (Manus), Meta controls the entire value chain.

Google has Jarvis. Microsoft has Copilot. But neither integrates directly into a 3-billion-user messaging ecosystem with established business infrastructure. If Meta's agents handle user intent and task execution directly within WhatsApp, they bypass traditional search engines entirely—threatening Alphabet's core ad business.

AI ROI Answer:

Meta's Q3 revenue surged 26% year-over-year to $51.2 billion, driven by AI-enhanced ad targeting. The company's forward P/E multiple has compressed to 22x—significantly cheaper than Alphabet at 28x and below historical averages. Strong cash flow supports one of Wall Street's biggest share repurchase programs.

Manus adds immediate commercial traction: $125 million revenue run rate provides proof that customers will pay for agentic AI. Meta can scale this across WhatsApp Business, Instagram business accounts, and enterprise tools, creating new revenue streams beyond advertising.

Analysts project that Manus integration could add meaningful revenue by 2026-2027, helping justify Meta's elevated AI spending. The acquisition signals Meta is building not just infrastructure but monetizable products.

The Bearish Case:

Meta is falling behind in the foundation model race. Llama 4 has underperformed expectations while Chinese models (Kimi, Qwen, DeepSeek) advance rapidly. The company faces uncertain returns on massive infrastructure investments:

Meta has stated that total expenses "will grow at a significantly faster percentage rate in 2026 than 2025" (official Q3 2025 guidance)

Capital expenditures raised to $70-72 billion for 2025

Higher depreciation and infrastructure costs compressing margins

Meta's Q3 earnings triggered an 11% stock decline as Oppenheimer and Benchmark downgraded shares, specifically citing capex concerns and challenging margin outlook. The multi-billion-dollar question remains: will costly AI enhancements translate to effective monetization?

Execution Risks:

Manus employs just 105 people and built its technology in 2-3 months using external models (Anthropic, Alibaba, OpenAI). The startup's lean approach contrasts sharply with Meta's infrastructure-heavy strategy. Integrating Manus into Meta's ecosystem—across WhatsApp, Instagram, Facebook, Messenger, and Meta AI—requires massive engineering resources and operational complexity.

The company also faces:

Slower monetization of new platforms (Threads at 350M MAU vs X's 580M MAU)

TikTok's U.S. revival creating competitive pressure

Regulatory scrutiny over the Manus acquisition's Chinese origins

Potential antitrust concerns from blocking third-party AI on WhatsApp

At ~$666 per share, META trades at valuations that assume flawless execution. Any integration delays, regulatory pushback, or competitive setbacks could compress multiples significantly.

What Flow Data Showed:

On December 19—when Bloomberg later confirmed deal negotiations began—institutional flow hit -$6.24 billion with a Z-score of -2.74 (99.7th percentile selling intensity). Retail was buying modestly that day, oblivious to what was happening behind closed doors.

When the deal was announced December 29, the stock gained just 1.4% despite $2+ billion in acquisition value and explosive growth metrics. This muted reaction reveals that institutions had already distributed ahead of the news.

The flow data captured when smart money positioned—approximately 10 days before the public announcement, around when negotiations likely started.

What the Flow Data Revealed

Let's look at what actually happened between December 8-31—and how institutions sold the news before it became news while retail provided exit liquidity.

Charts below.

Pattern: Institutional Pre-Positioning Meets Retail Post-Announcement Buying

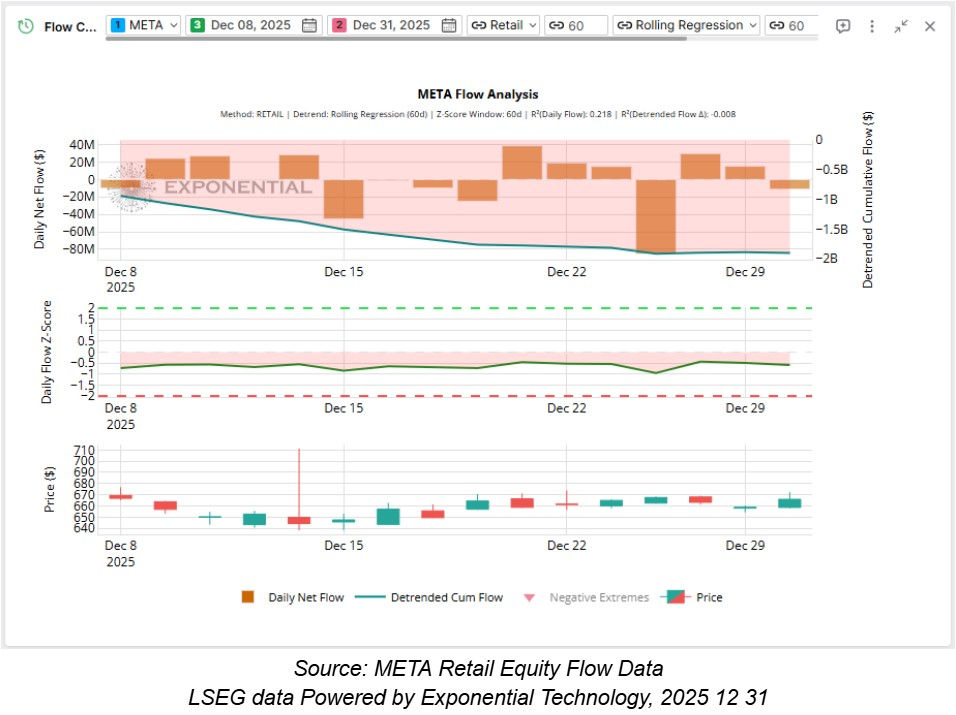

The Retail Story

December 8-23: Negative detrended cumulative flow develops. Retail sentiment turns cautious as META underperforms (+11% YTD vs peers). Daily flows oscillate between slightly negative and neutral.

December 15: Moderate negative daily net flow of -45M (2nd largest negative). Z-score hits -0.84. Retail taking some profits or reducing exposure.

December 24 (Tuesday): Massive retail selling. Daily net flow plunges to -85.2M (largest negative in the period) with Z-score dropping to -0.95. Holiday week profit-taking or de-risking ahead of year-end.

December 26-29: Retail flow turns moderately positive. Small accumulation as stock holds ~$660-670 range. Z-scores climb back toward neutral territory.

December 30 (Monday, day after announcement): Retail continues buying into the +1.1% gain. Flow remains positive as headline readers react to the acquisition news. But the magnitude is modest—retail missed the real opportunity.

Click to expand

The Institutional Story

Here's where it gets fascinating. Institutional flow tells a completely different—and far more informed—story:

December 8-11: Positive detrended cumulative flow. Institutions accumulating quietly. December 11 shows the period's most positive daily flow at +1.90B with Z-score +1.15.

December 12-16: Volatility increases. December 15 sees moderate accumulation. December 16 marks a turning point.

December 17: Second-largest negative daily flow at -2.18B with Z-score -0.93. Institutions testing distribution or beginning to de-risk.

December 18: Reversal. Second-largest positive flow at +1.64B with Z-score +0.98. Possible false rally to create exit liquidity or final positioning before major distribution.

December 19 (Thursday): MASSIVE DISTRIBUTION EVENT.

Institutional daily net flow: -6.24 billionZ-score: -2.74 (99.7th percentile)

This is 2.74 standard deviations above normal institutional selling—a statistical extreme that occurs roughly 0.3% of the time. This wasn't routine profit-taking. This was informed positioning.

Bloomberg later confirmed the Meta-Manus deal negotiations began "about 10 days" before the December 29 announcement. December 19 is exactly when those negotiations would have started.

The selling was deliberate, sustained, and massive. Institutions distributed $6.24 billion into retail and algorithmic buying, knowing a major announcement was imminent but not yet public.

December 22-23: Moderate institutional buying returns (+$700-780M). Small flows suggest institutions finished repositioning and are waiting for announcement.

December 24-29: Neutral institutional behavior. Daily flows moderate. Detrended cumulative flow stabilizes. Institutions sitting on their hands, waiting for public disclosure.

December 30 (Monday, announcement day): Stock gains 1.1% to $665.95. Institutional flow shows modest activity—no explosive buying, no major distribution. The move already happened December 19.

Click to expand

What This Actually Means

✅ Institutional pre-positioning (Dec 19): Massive distribution (-$6.24B, Z-2.74) around when deal negotiations likely began—approximately 10 days before public announcement

✅ Timing precision: The largest institutional selling event in the entire December period occurred around when Bloomberg later confirmed negotiations started (approximately 10 days before announcement)

✅ Information asymmetry: While retail sold moderately or stayed neutral through December 19-24, institutions distributed heavily on December 19

❌ Retail late to the story (Dec 30): Modest buying after public announcement, missing the real flow divergence from December 19

❌ Muted announcement reaction (+1.1%): Stock barely moved despite $2B+ deal and explosive Manus growth metrics—because institutions already priced it in December 19

✅ Magnitude dominance: December 19 institutional selling (-$6.24B) dwarfed retail activity throughout the entire period

✅ The critical insight: The modest +1.1% gain on December 30 despite transformative acquisition news reveals institutions had already repositioned approximately 10 days earlier

✅ Pre-announcement distribution vs post-announcement calm: Institutions distributed when deal negotiations started (Dec 19), then stayed quiet when the news dropped (Dec 30)

The Advance Warning

The flow data revealed a devastating sequence of informed institutional positioning versus retail reaction:

December 11-18: The Setup

Context: META trading in $660-670 range, up only 11% YTD (underperforming tech peers)

Institutional response: Large positive flow on December 11 (+$1.90B, Z+1.15), then volatility Dec 17-18 (-$2.18B, then +$1.64B)

Retail response: Moderate negative flows, cautious sentiment

Pattern: Institutions creating liquidity conditions for upcoming distribution event

December 19: The Distribution Event

Context: Deal negotiations begin "about 10 days" before December 29 announcement (per Bloomberg)

Institutional response: Explosive selling (-$6.24B, Z-2.74) representing 99.7th percentile of distribution intensity

Retail response: Not providing significant buying pressure—mostly neutral to slightly negative

Critical insight: Institutions distributed $6.24 billion around when negotiations likely started, not when news became public

This 2.74 standard deviation event means institutional selling was more extreme than 99.7% of all historical daily periods. This doesn't happen by accident.

December 24: Retail Capitulation

Context: Holiday week, year-end positioning

Retail response: Largest selling event of period (-$85.2M, Z-0.95)

Institutional response: Neutral behavior, finished repositioning

Retail mistake: Sold after institutions already distributed, missing that December 19 was the informed move

December 30: The Announcement

Context: Meta announces $2B+ Manus acquisition, fastest startup ever to $100M ARR (8 months), strategic shift to agentic AI

Stock response: +1.1% gain to $665.95 while S&P 500 -0.14%, Nasdaq -0.24%

Institutional response: Modest flows, no explosive reaction—the positioning already happened December 19

Retail response: Buying into the news after institutions already positioned

The Critical Difference:

Retail saw the sequence as:

December 19-24: Choppy market, year-end volatility → Caution or selling

December 30: Major acquisition announced → Buy the news

Institutions saw one strategic inflection:

December 19: Deal negotiations begin (internal information) → Distribute $6.24B at Z-2.74

December 30: Public announcement → Already positioned, modest +1.1% confirms pricing

The 99.7th percentile institutional selling on December 19—coinciding with when Bloomberg later confirmed negotiations started (approximately 10 days before announcement)—showed who had information and when they likely acted on it.

Retail was trading price action.

Institutions were trading negotiations.

What Makes LSEG Equity Flow Data Different

1. Granularity

Minute-level intervals with 17 years of historical data. For META, the daily view showed the critical December 19 distribution event (-$6.24B at Z-2.74) occurring around when deal negotiations likely began—approximately 10 days before public announcement.

When you need deeper insight into intraday dynamics—like understanding exactly when during the December 19 session institutional distribution accelerated, or precisely when on December 30 flows responded to the announcement—the minute-level data is there.

2. Segmentation

Multiple high-frequency inference methods separate institutional from retail, market makers from informed traders. You know exactly who's moving into and out of a stock—and why it matters.

In META's case, this segmentation revealed the devastating information asymmetry: institutions distributed massively on December 19 (-$6.24B, Z-2.74) around when negotiations likely started, while retail activity remained neutral to negative. Without segmentation, you'd see December 19 net selling and miss that institutions drove it with informed positioning.

You'd see December 30's modest +1.1% gain and think the market was pricing in the news—missing that institutions already distributed approximately 10 days earlier when the information became available to them.

3. Breadth

All US listed equities across all trading venues. No blind spots in coverage. Whether you're tracking mega-cap tech names making multibillion-dollar acquisitions or emerging AI startups transitioning to strategic assets, the data is comprehensive.

4. Real-Time Intelligence

See accumulation and distribution patterns as they develop—not after the price has already moved. META's December 19 institutional distribution (-$6.24B, Z-2.74) was visible in real-time to those with access to flow data.

When the December 29 announcement triggered a modest +1.1% gain despite transformative news, the message was unmistakable: institutions sold the news before it was news. The information was already priced in.

The Bigger Picture: When AI Acquisitions Meet Geopolitical Complexity

META perfectly encapsulates the current AI investing dynamic:

Fundamentals: Strong Q3 revenue growth (+26% YoY to $51.2B), AI-enhanced ad targeting delivering results

Valuation: Forward P/E compressed to 22x (vs Alphabet at 28x), below historical averages despite elevated growth

Strategic Position: Shifting from conversational chatbots (Meta AI) to agentic AI (Manus) for monetization

Geopolitical Complexity: Acquiring Chinese-founded startup, buying out all Chinese investors, discontinuing China operations to satisfy U.S. regulators

Deal Speed: Negotiations struck in "about 10 days"—one of fastest major tech M&A transactions

Market Structure: Institutional pre-positioning (Dec 19, Z-2.74) versus retail post-announcement reaction (Dec 30)

In this environment, understanding timing matters more than understanding fundamentals. Knowing that Manus is transformative (fastest to $100M ARR, 8 months) doesn't help if you buy after institutions already distributed when negotiations began.

Real-time flow intelligence tells you:

When institutions receive information (Dec 19: deal negotiations start)

How they act on that information (Dec 19: -$6.24B distribution at Z-2.74)

When retail discovers the story (Dec 30: public announcement)

Why price reactions are muted (Dec 30: +1.1% because already priced in from Dec 19)

When to maintain conviction despite modest moves (Understanding distribution happened 10 days early)

META's situation shows that in today's market, trading on public announcements causes you to miss when informed capital repositions. Retail saw a December 30 acquisition to evaluate. Institutions saw December 19 negotiations to act on.

When institutions distributed $6.24B at Z-2.74 on December 19—around when negotiations likely started—then stayed quiet when the announcement dropped on December 30, the message was clear: retail was trading headlines, institutions were trading information flow.

The Way Forward

Option 1: The Old Way

Keep trading on price action and public announcements. Buy into transformative acquisitions after they're announced. Accept that your entry timing will match headline readers—which means entering after institutions already positioned.

Watch stocks barely move on major news because you missed when informed capital acted. React to +1.1% gains without understanding that the real distribution happened approximately 10 days earlier during private negotiations. Assume all acquisition announcements are equal and trade them identically.

Option 2: The New Way

Get visibility into who's moving and when through real-time flow segmentation. Understand that when institutions distribute $6.24 billion at Z-2.74 (99.7th percentile) on December 19, and Bloomberg later confirms deal negotiations started "about 10 days" before the December 29 announcement, this isn't coincidence—it's information asymmetry.

Recognize that when a $2+ billion acquisition of the fastest-growing startup in history (Manus: $100M ARR in 8 months) generates only a +1.1% stock move, institutions already priced it in through December 19 distribution. Position strategically based on how informed capital responds in real-time, not based on press releases alone.

In META's case, the flow data showed exactly what was happening:

✅ December 19: Massive institutional distribution (-$6.24B, Z-2.74) around when deal negotiations likely began

✅ December 30: Modest price reaction (+1.1%) despite transformative news—because positioning already happened

❌ Retail timing: Buying after public announcement, missing December 19 informed distribution

✅ The signal: 99.7th percentile institutional selling around when negotiations likely started = information asymmetry

You could have:

Recognized December 19 institutional distribution (Z-2.74) as informed positioning ahead of major catalyst

Understood the magnitude (-$6.24B) represented 99.7th percentile selling intensity—not routine profit-taking

Connected the timing (December 19) to Bloomberg's later confirmation that negotiations began "about 10 days" before announcement

Anticipated that December 30's modest +1.1% reaction reflected pre-positioning, not fair value discovery

Avoided buying the December 30 headline when institutions already distributed December 19

Understood that fastest-to-$100M-ARR startup + $2B+ acquisition + geopolitical complexity = major information event institutions would front-run

The information was there. The question is: were you looking?

Stop Reacting. Start Anticipating.

The debate over META's AI strategy will continue.

Bulls will point to Manus's WhatsApp monetization potential, $125M revenue run rate, and perfect SMB fit transforming messaging from cost center to profit engine.

Bears will highlight $70-72B capex, $155B operating expenses, uncertain foundation model competitiveness, and execution risks integrating 105-person startup into billion-user platforms.

But with real-time flow intelligence, you don't have to guess which thesis will win. You can see exactly when deal negotiations trigger institutional distribution, when informed capital repositions ahead of announcements, and when headline reactions are already priced in—and trade accordingly.

The December 19-30 sequence wasn't random:

Dec 19: Institutional distribution (-$6.24B, Z-2.74) when negotiations began

Dec 30: Modest reaction (+1.1%) despite $2B+ deal—because positioning already happened

Institutions understood immediately: when you're negotiating to acquire the fastest-growing AI startup in history (8 months to $100M ARR), with Chinese founders requiring complete buyout of Chinese investors, and completing negotiations in 10 days, that information creates trading opportunities before the press release.

Want to see how this works for your portfolio?

LSEG Equity Flow data, Powered by Exponential Technology, integrates institutional-grade flow analytics with AI-powered pattern recognition. We'll show you exactly what you're missing.

📧 Questions? Email: sales@exponential-tech.ai

📅 Book a Demo: See institutional flows in real-time

Your competition isn't waiting. Why are you?

About LSEG Equity Flow Data

LSEG Equity Flow data, Powered by Exponential Technology, is based on the US Consolidated Feed and applies deep high-frequency trading knowledge to identify the direction of active risk-taking by institutional buy-side, market makers, and retail traders. With unprecedented 1-minute granularity and 17 years of history, the dataset provides a unique ability to distinguish institutional and retail flow, providing near-real-time market intelligence across the entire US equity market.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Past performance does not guarantee future results. Flow data provides intelligence on positioning but cannot predict all market outcomes.

Comments